Table of Contents

ToggleBiometric authentication in banking is the use of unique physical traits — most commonly a fingerprint or a face scan — to confirm a customer’s identity when they open an account, sign in, or authorize a payment. Instead of relying on passwords and PINs that can be phished, guessed, or leaked, banks and fintechs verify who the user is. The result is faster onboarding, stronger fraud prevention, and compliance built into the customer journey rather than bolted on afterwards. This guide explains how face and fingerprint recognition work in financial services, where they deliver the most value — from remote KYC to passwordless login — and what regulators expect when banks handle biometric data.

Learn how Identy.io strengthened mobile security in the banking sector with advanced fingerprint biometrics and seamless user experience.

What is biometric authentication in banking?

At its core, biometric authentication answers a simple question: is this really the right person? A sensor captures a biometric sample, software converts it into an encrypted mathematical template, and that template is compared against a stored reference. When the two match within a defined threshold, access is granted.

It helps to separate two terms that are often confused. Verification is the one-time check, usually at onboarding, that a person is who they claim to be. Authentication is the recurring confirmation of that identity every time the customer logs in or approves a transaction. Both rely on the same underlying biometric technology, applied at different points in the relationship.

Three modalities dominate in finance. Facial biometric authentication uses the geometry of a face and is ideal for camera-based mobile flows. Fingerprint recognition captures the ridge patterns of a finger, increasingly through the smartphone camera itself rather than a dedicated scanner. Behavioral biometrics, a newer layer, analyzes patterns such as typing rhythm or how a device is held to spot anomalies passively during a session.

Biometric onboarding and KYC in banking

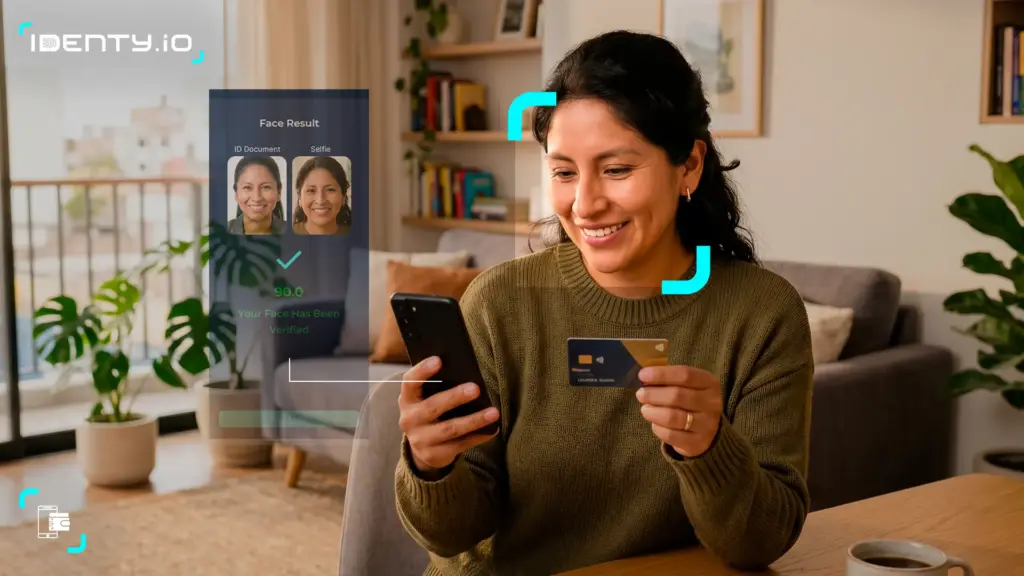

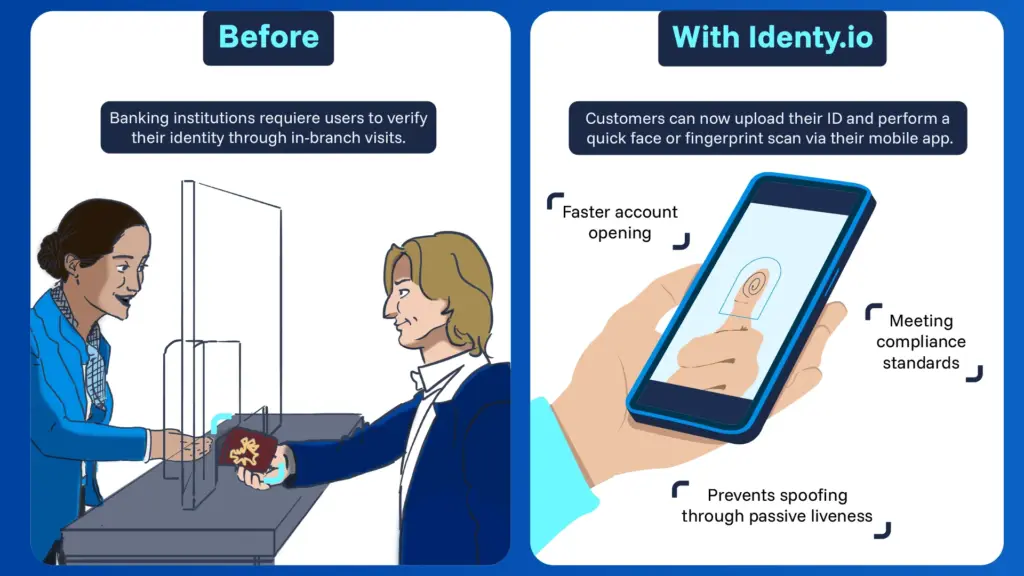

The clearest win for biometrics is onboarding. Traditional Know Your Customer procedures required customers to visit a branch and wait days for manual review. Biometric KYC compresses that into minutes: the customer photographs an ID document and performs a quick face or fingerprint scan from their phone, and the system matches the live capture against the document or a trusted database.

A critical safeguard in this flow is liveness detection, which confirms that a real, present person is being scanned rather than a printed photo, a video replay, or a deepfake. This is what makes remote biometric identity verification trustworthy enough to satisfy Anti-Money Laundering (AML) obligations without a face-to-face meeting.

The benefits compound for both sides:

- Speed: accounts opened in minutes instead of days, reducing drop-off during sign-up.

- Security: liveness and anti-spoofing block presentation attacks at the door.

- Inclusion: customers without easy access to a branch can verify their identity securely from anywhere.

This is not theoretical. Identy.io’s fingerprint technology was deployed to validate customer fingerprints remotely and eliminate branch visits during onboarding — a shift documented across our customer success stories, where institutions extended secure banking access to thousands of users who previously faced friction at every step.

Fraud prevention through biometrics

As fraudsters adopt deepfakes, stolen credentials, and synthetic identities — profiles stitched together from real and fabricated data — static checks alone no longer hold. Biometric verification raises the bar by tying every action to a living person rather than to a reusable secret.

By comparing a real-time face or fingerprint against a document or proprietary database, institutions can confirm that a genuine individual — not an AI-generated replica — is behind an onboarding session or a transaction. Industry analysts consistently flag synthetic identity fraud as one of the fastest-growing threats to lenders, which is why biometric defenses are moving from optional to standard.

Beyond one-off checks, behavioral biometrics adds a continuous layer. By learning how a user normally types, swipes, or holds a device, these systems flag deviations mid-session and trigger step-up authentication without disrupting legitimate customers. Combined, face, fingerprint, and behavioral signals create a multi-factor ecosystem that is far more resistant to impersonation than any single control.

Authentication beyond passwords

In day-to-day banking, biometrics have become a primary authentication factor. Customers open their banking app or approve a payment with a face or fingerprint scan, removing the password from the equation entirely. The payoff is both experiential and defensive: frictionless logins on one hand, and strong protection against phishing and credential theft on the other, since there is no static secret to steal.

This aligns directly with regulation. Under the EU’s PSD2 directive, Strong Customer Authentication (SCA) requires two of three independent factors — knowledge, possession, and inherence. Biometrics satisfy the inherence factor, which is why major banks and fintechs have folded face and fingerprint checks into login and high-risk actions. For mobile-first institutions, biometric authentication is now a competitive differentiator as much as a security measure.

Biometric use cases in banks

The same technology supports a wide range of digital identity verification use cases across the institution:

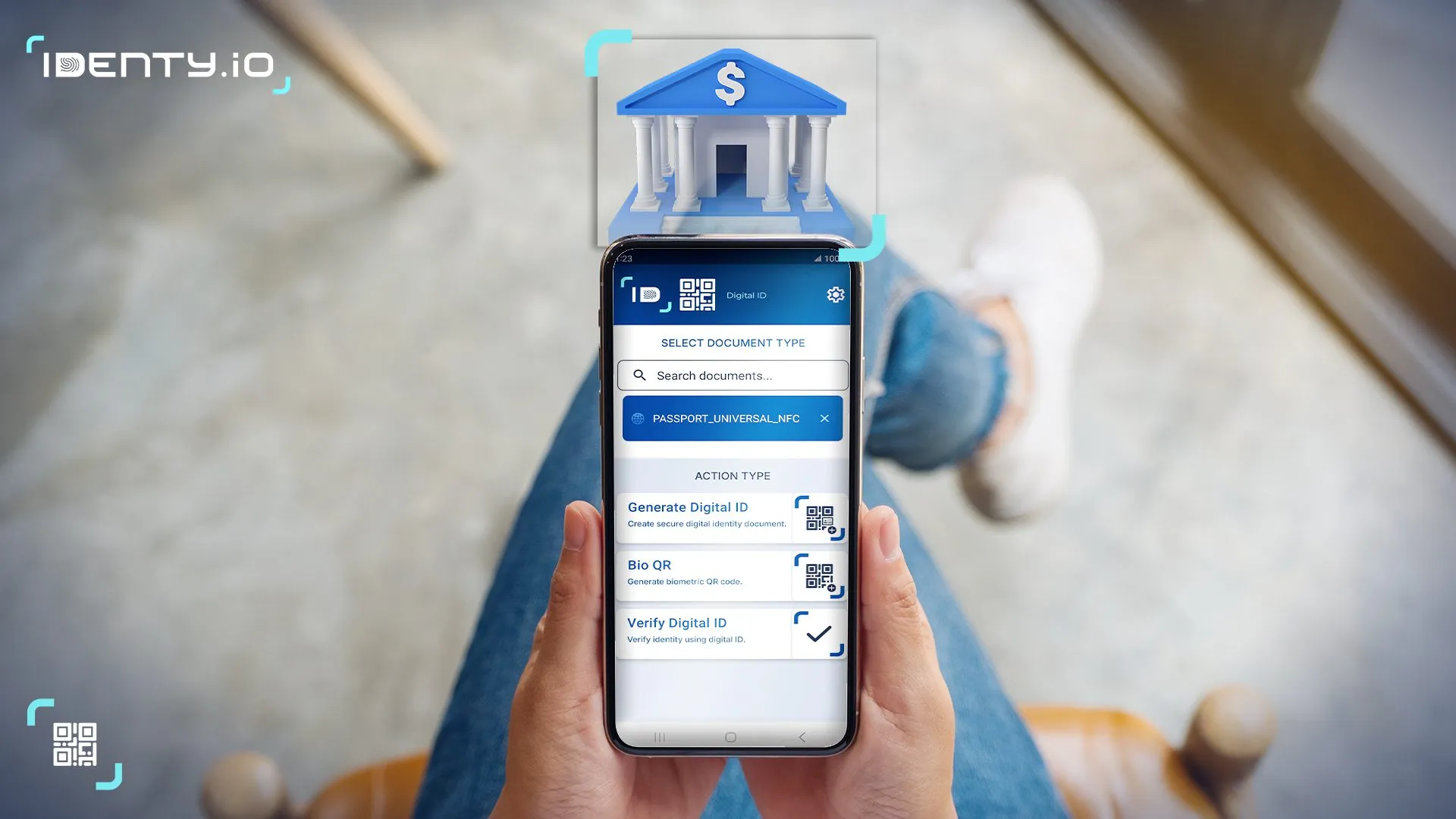

- Remote account opening — verify new customers end-to-end without a branch visit.

- Bank biometric verification at login — replace passwords with face or fingerprint sign-in.

- Transaction authorization — confirm high-value or high-risk payments with a live scan.

- Account recovery — restore access securely without knowledge-based questions that fraudsters can research.

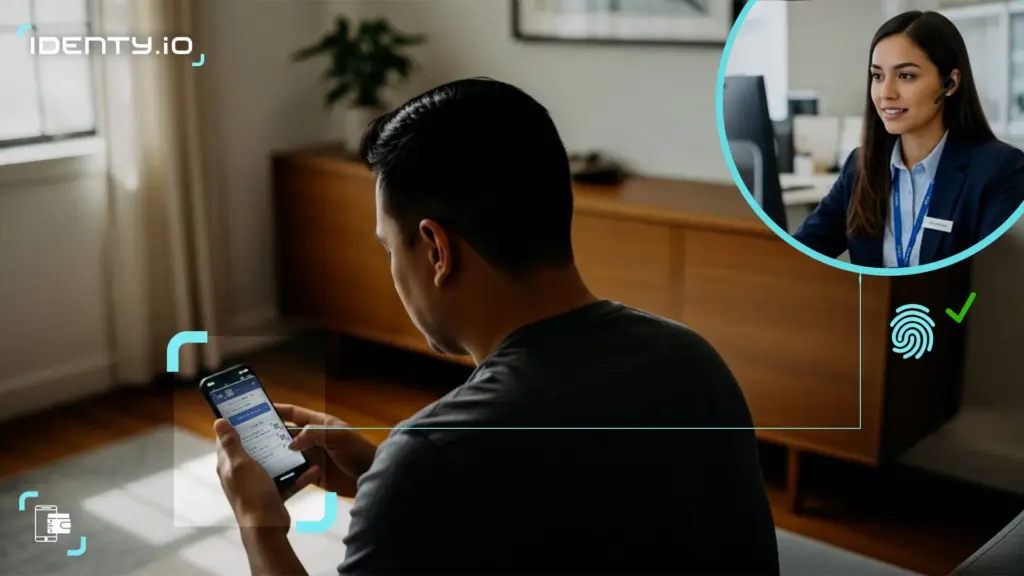

- Branch and ATM identification — authenticate customers in person where supported.

- Step-up authentication — add a biometric check only when risk signals warrant it.

Because each use case draws on the same ID verification software, banks can standardize identity assurance across channels instead of maintaining disconnected tools.

Face vs fingerprint vs other biometric modalities

No single modality is right for every scenario. The table below summarizes how the main options compare for banking use.

| Modality | Typical use | Strengths | Considerations |

|---|---|---|---|

| Facial recognition | Mobile onboarding, app login | Fast, contactless, works with any front camera | Needs robust liveness against deepfakes; lighting sensitivity |

| Fingerprint | Onboarding, login, payment approval | Highly distinctive; capturable via smartphone camera | Capture quality varies with worn or wet fingers |

| Behavioral biometrics | Continuous, in-session monitoring | Passive, frictionless, hard to imitate | Probabilistic; best as a complementary layer |

In practice, leading institutions combine modalities — a face or fingerprint at the gate, behavioral signals during the session — to balance security and user experience.

Compliance and privacy in biometric banking

Biometric data is classified as sensitive personal information, and handling it carries specific obligations. Under the EU’s GDPR and the U.S. Biometric Information Privacy Act (BIPA), institutions generally need explicit, informed consent and a clear basis for processing, alongside secure storage and defined retention limits.

The privacy-by-design answer most banks adopt is to store biometric data as encrypted templates rather than raw images, and increasingly to keep those templates on the user’s own device rather than in a central database. This minimizes the blast radius of any breach: a stolen template is an irreversible mathematical artifact, not a usable face or fingerprint. Done well, biometric banking improves both security and privacy at the same time.

The future of banking is biometric

As fintech ecosystems mature, biometric identification is set to underpin every stage of the customer journey, from the first onboarding scan to daily authentication and payment approval. The institutions pulling ahead are those treating identity as a continuous, biometric-first capability rather than a one-time gate.

For banks weighing the move, the practical starting point is a single, well-integrated identity layer. Explore how Identy’s biometric software for banks and financial institutions brings face and fingerprint verification together under one compliant, on-device framework.

Frequently asked questions

What is biometric authentication in banking?

It is the use of unique physical traits, such as a fingerprint or face scan, to confirm a customer’s identity when opening an account, logging in, or authorizing a transaction — replacing or reinforcing passwords and PINs.

How does biometric authentication work in banks?

A sensor captures a face or fingerprint, converts it into an encrypted template, and compares it against a stored reference. A match within a set threshold authenticates the user, while liveness detection confirms a real person is present.

What is biometric KYC?

Biometric KYC verifies identity by matching a live face or fingerprint against an ID document or trusted database, letting banks onboard customers remotely in minutes while meeting AML requirements.

What is the difference between biometric authentication and verification?

Verification is the one-time check at onboarding that a person is who they claim to be. Authentication is the recurring confirmation of that identity each time they log in or approve an action.

Is biometric authentication safe for banking?

Yes, when implemented well. Encrypted templates, on-device storage, and liveness detection make biometrics harder to steal or reuse than passwords, which can be phished or leaked.

Can biometric data be stolen or spoofed?

Templates are encrypted mathematical representations, not images, so a leaked template cannot be turned back into a usable fingerprint or face. Liveness and anti-spoofing defend against photos, masks, and deepfakes.

Is biometric authentication PSD2 and SCA compliant?

Yes. Biometrics qualify as the inherence factor for Strong Customer Authentication under PSD2, satisfying one of the two required factors alongside possession or knowledge.

Bibliography

- European Union. Regulation (EU) 2016/679 (GDPR) — Articles 4 and 9 on personal data and special categories, including biometric data. eur-lex.europa.eu

- European Union. Directive (EU) 2015/2366 (PSD2) — Strong Customer Authentication requirements. eur-lex.europa.eu

- European Commission. Commission Delegated Regulation (EU) 2018/389 — EBA Regulatory Technical Standards on SCA and common secure communication. eur-lex.europa.eu

- State of Illinois. Biometric Information Privacy Act (BIPA), 740 ILCS 14 (2008). ilga.gov

- ISO/IEC 30107-3 — Information technology — Biometric presentation attack detection (liveness detection). iso.org

- ISO/IEC 24745 — Information technology — Security techniques — Biometric information protection (template protection). iso.org

- NIST. SP 800-63 Digital Identity Guidelines — identity proofing and authenticator assurance levels. pages.nist.gov

- FIDO Alliance. Passwordless and biometric authentication standards. fidoalliance.org