Table of Contents

ToggleDigital identity theft prevention and protection

Identity theft remains a growing threat for financial and government services, challenging digital trust and user experience. In 2024 U.S. authorities received over 1.1 million identity-theft reports, underscoring the scale of the problem. New fraud patterns (e.g. tax-refund schemes, synthetic identities, AI-driven deepfakes) demand advanced solutions. This report examines risk trends and regulatory context, and outlines a layered defense strategy: strong biometric authentication, real-time fraud analytics, and user-centric protections (like credit monitoring and insurance). For example, Identy.io (a FIDO Alliance member) offers a touchless mobile biometric platform with built-in liveness checks, illustrating how modern identity verification can enhance security without sacrificing usability. Ultimately, financial firms must balance security and convenience to prevent identity theft and preserve customer trust.

Deepfakes are becoming more sophisticated, increasing the risk of fraud and identity manipulation in digital environments. Download our 10-step guide to learn how to detect threats early and protect your organization with proven best practices.

Identity theft trends and risks

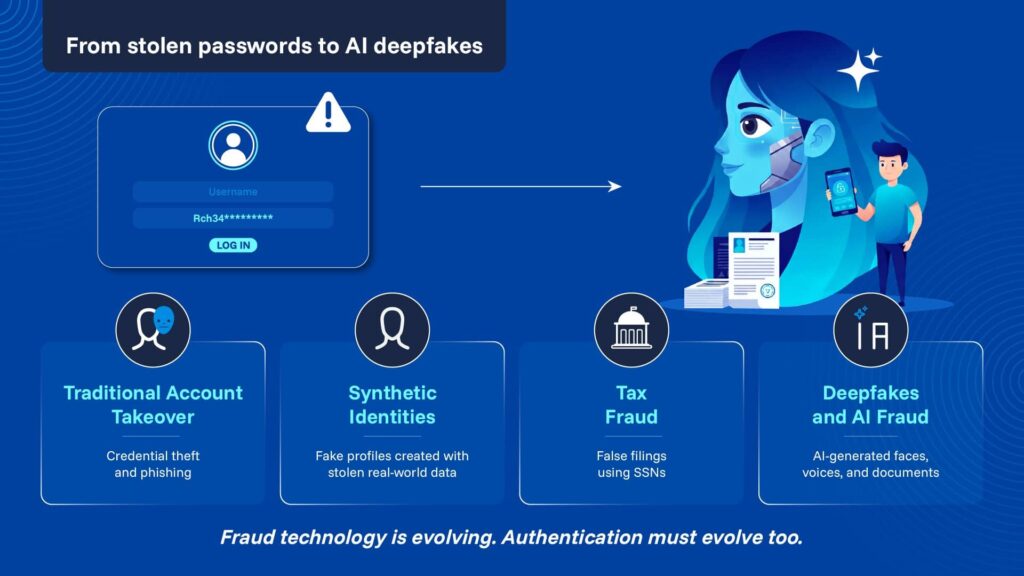

Identity theft occurs when attackers misuse personal data to gain illicit access to accounts or benefits. Victims can suffer financial loss and damaged credit, while institutions face fraud losses and reputational damage. Beyond traditional account takeovers, criminals increasingly use synthetic identities (fabricating profiles from stolen data) and commit tax-related fraud. In tax schemes, for example, thieves file bogus returns with stolen Social Security numbers to claim refunds. The IRS provides a dedicated affidavit (Form 14039) to report such tax-related identity theft.

The scale of identity fraud is large and rising. In 2024 U.S. authorities received over 1.1 million identity theft reports. Fraudsters are also exploiting new channels: account breaches often lead to social engineering attacks and multi-layer fraud. As one industry analysis notes, “Fraud is evolving faster than ever, with AI-powered scams [and] deepfake-enabled identity theft” targeting financial institutions. This trend emphasizes that how to prevent identity theft must include vigilance against emerging AI-driven impersonation. Financial leaders should treat identity theft not just as a compliance box but as a business risk: loss of customer trust and potential regulatory fines (e.g. under data protection laws) can hurt the bottom line.

Deepfakes and AI-Driven Fraud

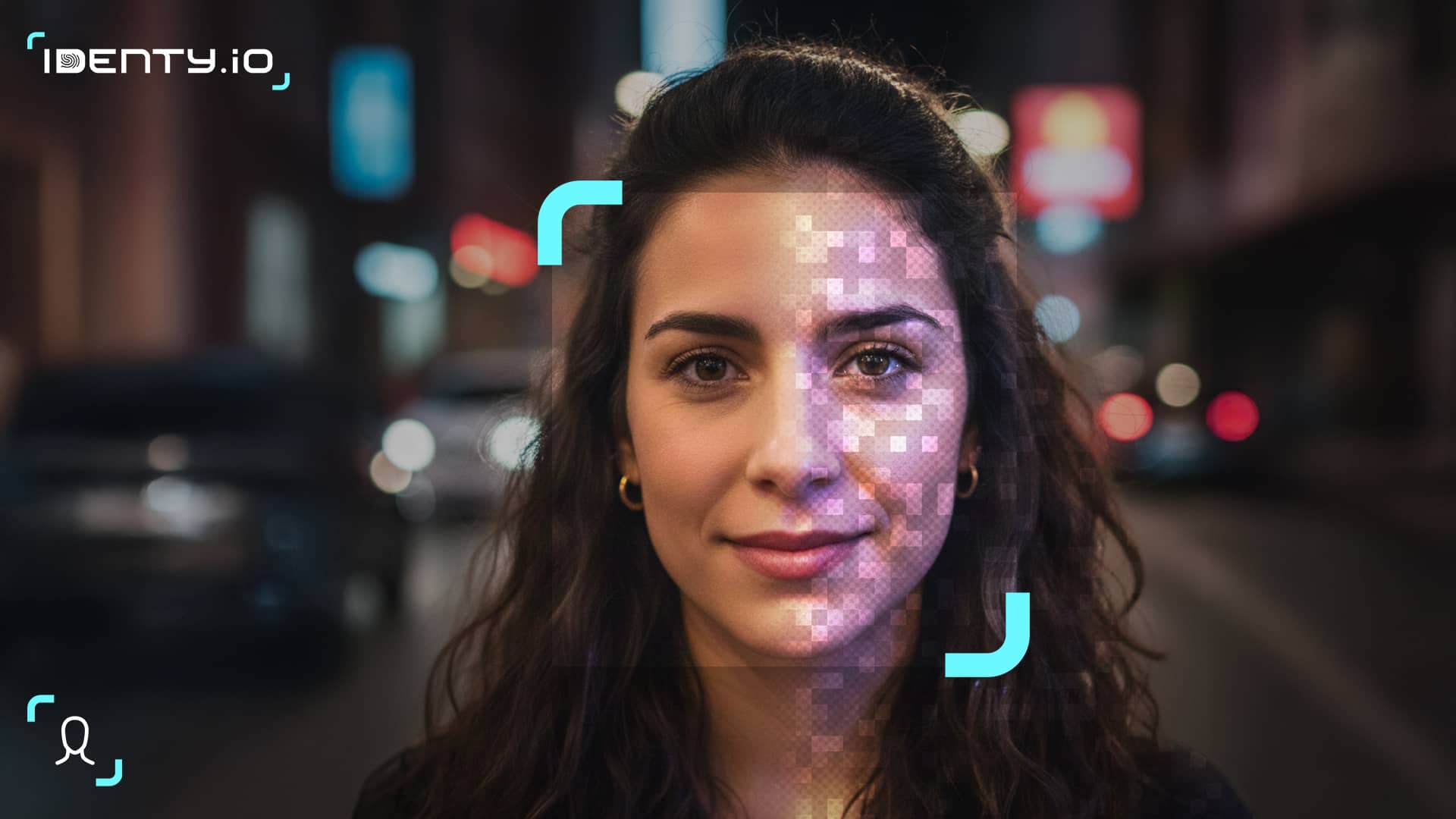

Deepfake attacks are an emerging vector in identity crime. Advances in AI allow fraudsters to generate synthetic faces, voices, or documents that impersonate real customers. The pace of deepfake-enabled fraud has outrun most identity verification systems built even three years ago. AI-generated faces, voice clones, and synthetic documents now appear in financial onboarding attacks at scale — and the tools to create them are freely available online.. These AI-enabled forgeries can defeat naive camera-based checks.

To counter such threats, organizations deploy deepfake detection software and liveness solutions. Modern systems analyze video streams for signs of tampering, using passive AI techniques — analyzing skin texture, natural micro-movements, 3D depth, and light diffusion — that run invisibly in the background to ensure the user is genuine. No prompts. No instructions. No friction. For example, robust liveness detection “provides temporal data that helps systems identify inconsistencies between genuine and fraudulent attempts”. Incorporating AI-based deepfake detection in onboarding and transaction authentication is thus becoming a business imperative. By adding these advanced checks, a fintech can block spoofed biometrics and synthetic IDs before they lead to fraud.

Get a tailored demo of our contactless biometric platform and see how it fits your specific use case.

Biometric solutions and digital trust

Strong biometric solution authentication is a key layer of identity theft prevention. Biometric factors (fingerprint, face, iris) tied to user devices resist common attacks like phishing or stolen credentials. The FIDO Alliance champions such approaches, noting that migrating to passwordless methods is critical as traditional passwords “are coming under increasing scrutiny” in the face of modern fraud.

Identy.io exemplifies this trend. Identy.io is a FIDO-certified platform providing touchless mobile biometrics: it can verify users by scanning fingerprints on a smartphone camera, ensuring high performance and multi-finger liveness. According to U.S. NIST, “Identy.io provides mobile touchless biometrics technology and solutions for identity assertion in various markets, including financial services… and government services”. In practice, this means users can authenticate quickly (improving UX) while banks get cryptographically-strong proof of identity. By adopting FIDO-compliant biometrics, institutions reduce reliance on passwords and add a robust phishing-resistant factor. The result is both higher security and a smoother customer experience – a crucial business advantage in competitive fintech markets.

What sets Identy.io apart architecturally is where the processing happens. Every biometric check — capture, liveness analysis, matching — runs locally on the user’s smartphone. No biometric data leaves the device. For an article about identity theft prevention, this matters enormously: a system that never transmits biometric templates to a server eliminates an entire category of breach risk. Banks and governments deploying Identy don’t just verify identity more accurately — they verify it more safely.

Prevention strategies and compliance

A comprehensive identity theft prevention strategy is multi-layered. Key elements include data security, fraud monitoring, and customer education. In the U.S., many financial entities are already required by law to have a written identity theft prevention program (the Red Flags Rule). This means banks and lenders must regularly assess risk and implement procedures to spot suspicious activity on accounts. In the EU and UK, regulations like eIDAS 2.0 and PSD2 require strong customer authentication for digital payments and are driving adoption of digital identity wallets with biometric verification. In Latin America — a primary market for mobile biometric deployments — Brazil’s LGPD and Mexico’s regulatory frameworks have introduced KYC and data protection requirements that effectively mandate advanced biometric checks for government services and online banking. Across all these regions, the compliance thread is the same: passive biometric liveness detection, validated to ISO 30107-3, now satisfies requirements that legacy knowledge-based authentication (KBA) cannot meet.

Beyond compliance, risk transfer tools add another safety net. Many institutions and credit-card networks offer identity theft protection services, often bundling credit monitoring with insurance. In fact, after major breaches the FTC has highlighted consumer benefits: for example, a settlement provided free credit monitoring plus up to $1 million in identity-theft insurance for victims. Such insurance reimburses consumers (or firms) for losses and recovery costs if fraud occurs, aligning incentives to mitigate risk. Additionally, firms should support victims with fraud-resolution services (e.g. identity restoration). On the policy side, governments provide victim tools: the IRS issues Identity Protection PINs to prevent tax fraud, and issues notice letters (e.g. Letter 5071C) when it detects suspicious tax returns.

By contrast, a failure to invest in these measures invites loss. Weak onboarding or lax controls can lead to costly account takeovers or fines. For digital platforms serving millions, even a small fraud rate hurts digital trust and profitability. Therefore, executives should ensure their IT teams deploy technologies like deepfake detection software, FIDO-based biometrics (e.g. Identy.io’s solution), and continuous analytics. They should also review insurance offerings and educate customers on safe practices. Taken together, these steps form the best identity theft protection posture: one that deters thieves and reassures regulators and users alike.

Get a tailored demo of our contactless biometric platform and see how it fits your specific use case.

Identity theft is an evolving challenge that sits at the intersection of security, compliance, and customer experience. As fraudsters deploy AI and social engineering, fintech and banking leaders must respond with a strategic, layered defense. This means combining passive liveness-certified biometrics (like Identy.io’s ISO 30107-3 Level 2 validated platform — the only mobile-first vendor achieving this with full on-device processing), real-time fraud monitoring, and user-focused safeguards (education, insurance). It also means aligning with regulations (Red Flags programs, PSD2 SCA) and industry standards to stay ahead of threats. The payoff is twofold: stronger protection against costly breaches, and a strengthened digital trust that customers value.

In the long run, organizations that prioritize identity theft prevention will differentiate themselves. Robust authentication and clear recovery processes can become selling points (“zero-trust security”, “fraud-first design”) that attract customers and partners. Conversely, neglecting identity risk invites brand damage and financial loss. Therefore, a business-oriented conclusion is clear: invest in scalable, user-friendly identity-proofing (e.g. mobile biometrics, liveness checks) and foster a culture of security. By doing so, institutions not only comply with rules but also unlock growth, because in financial services, trust earned through secure identity management is a key competitive advantage.

Bibliography

Biometric Update | Biometricupdate.com

Fido Alliance | https://fidoalliance.org/company/Identy.io/

FTC Gov | https://www.ftc.gov/business-guidance/privacy-security/red-flags-rule

IRS Gov | https://www.irs.gov/identity-theft-central/identity-theft-guide-for-individuals